Let’s say that our example company turned over the $2,200 accounts receivable to a collection agency on March 5, 2019 and received only $500 for its value. The difference between $2,200 and $500 of $1,700 is the factoring expense. Interest revenue from year one had already been recorded in 2018, but the interest revenue from 2019 is not recorded until the end of the note term. Thus, Interest Revenue is increasing (credit) by $200, the remaining revenue earned but not yet recognized.

- A customer will issue a note receivable if for example, it wants to extend its payment terms on an overdue account with the business.

- Notes Receivable is increased on the debit (left) side of the account and decreased on the credit (right) side of the account.

- Likewise, the company needs to calculate the note’s present value which is its fair value at the present date before it can make the journal entry for the non-interest-bearing note receivable.

- Essentially, in all these situations, the company that owns the receivable either sells it to the bank (or another lender) or borrows against it to obtain immediate cash.

Notes and Adjusting Entries

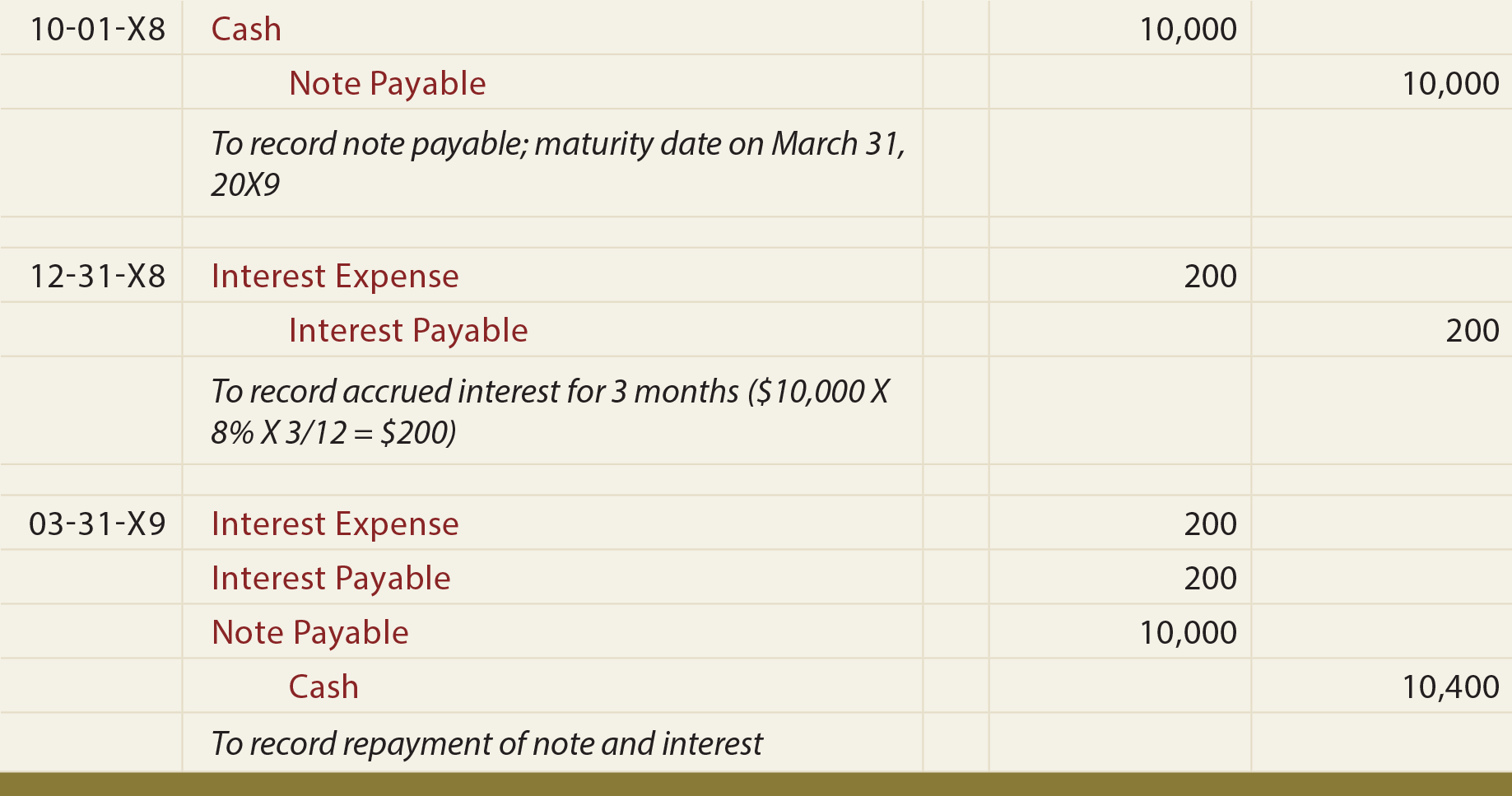

All financial assets are to be measured initially at their fair value which is calculated as the present value amount of future cash receipts. Cash payments can be interest-only with the principal portion payable at the end or a mix of interest and principal throughout the term of the note. Both parties agree that the customer must reimburse the principal amount and a 10% interest on the note. The maker of the note receivable, along with a principal amount, must also pay interest on it. The principal amount of the note receivable represents its face value or the value that the payee will receive. The maturity date of a note receivable is the date on which the final payment is due.

Notes receivable accounting:

The payee holds the note and is, therefore, due to receive a payment from the payer. The payer, or the marker, is the borrower who gets the loan from the payee. A note receivable will mention the two parties involved, the payee and the payer. The payee is the party that provides the loan, also known as the borrower.

Get in Touch With a Financial Advisor

It is similar to the maturity date of loans, representing a future point at which the borrower will repay the lender. When interest is due at the end of the note (24 months), the company may record the collection of the loan principal and the accumulated interest. The first set of entries show collection of principal, followed by collection of the interest. There are several elements of promissory notes that are important to a full understanding of accounting for these notes. These are the note’s principal, maturity date, duration, interest rate, and maturity value.

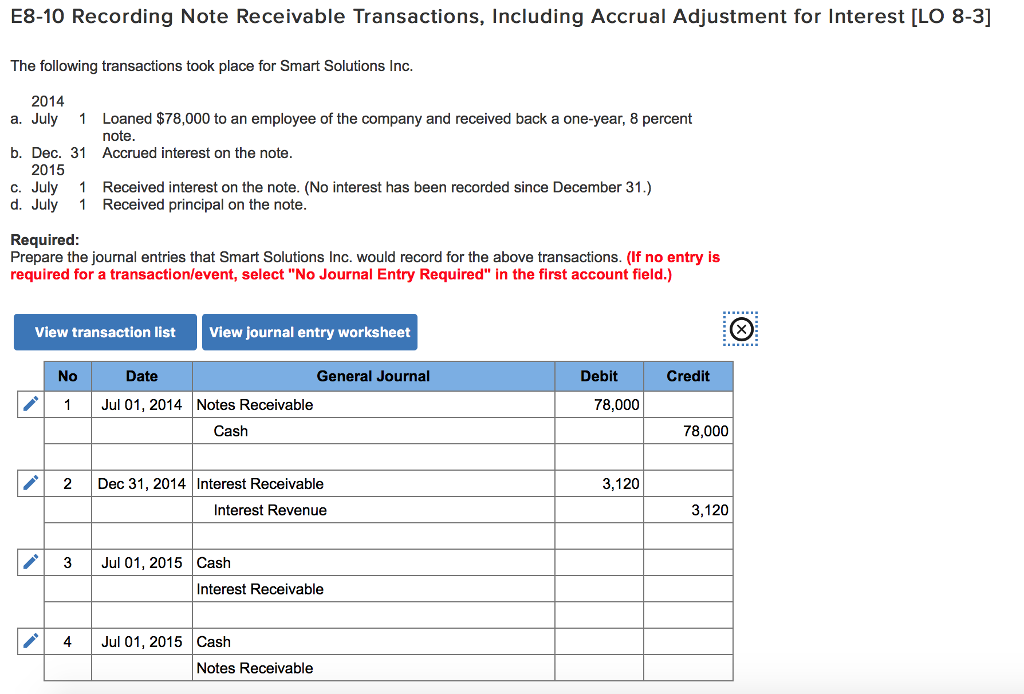

Example of Notes Receivable Accounting

By this time, the balance of note receivable will equal $10,000 ($9,754.11 + $81.28 + $81.96 + $82.64) which equals to the face value of the note. Notice that the sign for the $7,835 PV is preceded by the +/- symbol, meaning that the PV amount is to have the opposite symbol to the $10,000 FV amount, shown as a positive value. This invoice templates for free is because the FV is the cash received at maturity or cash inflow (positive value), while the PV is the cash lent or a cash outflow (opposite or negative value). Many business calculators require the use of a +/- sign for one value and no sign (or a positive value) for the other to calculate imputed interest rates correctly.

For example, a $1,000 non-interest-bearing note maturing in 3 months will have a value less than $1,000 today. After all, this $1,000 non-interest-bearing promissory note would simply imply that the issuer promises to pay $1,000 after 3 months. And that’s it; no interest nor any financial value is added to this $1,000 amount at all. That is why the company needs to discount the face value of the non-interest-bearing note which is the maturity value or the future value of the note to the present date before it can be recorded on the balance sheet. This is the concept of the time value of money where the money today is more valuable than the same money receiving in the future.

This balance represents 89 days [30 days in January, 28 days in February, 31 days in March] of the the 90 day note. Accounts Receivable is a normal business transaction for between a company and its customer. The intent is for the debt to be settled in the normal course of business, usually in 30 days (depending on the terms of the account.) It typically does not have an interest rate.

Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. The Bullock Company’s journal entries for 1 November 2019, 31 December 2019, and 31 January 2020 are shown below. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting. In our last article (found here), we reviewed how Notes Receivable are measured.

Consult your calculator manual for further instructions regarding zero-interest note calculations. Characteristically, notes are similar to loans because they come with interest and principal amounts. The accounts receivable is just as valid a claim as are the notes receivable, as well as the interest. In some cases, the note is received in one accounting period and collected in another.

Remember from earlier in the chapter, a note (also called a promissory note) is an unconditional written promise by a borrower to pay a definite sum of money to the lender (payee) on demand or on a specific date. A customer may give a note to a business for an amount due on an account receivable or for the sale of a large item such as a refrigerator. Also, a business may give a note to a supplier in exchange for merchandise to sell or to a bank or an individual for a loan.