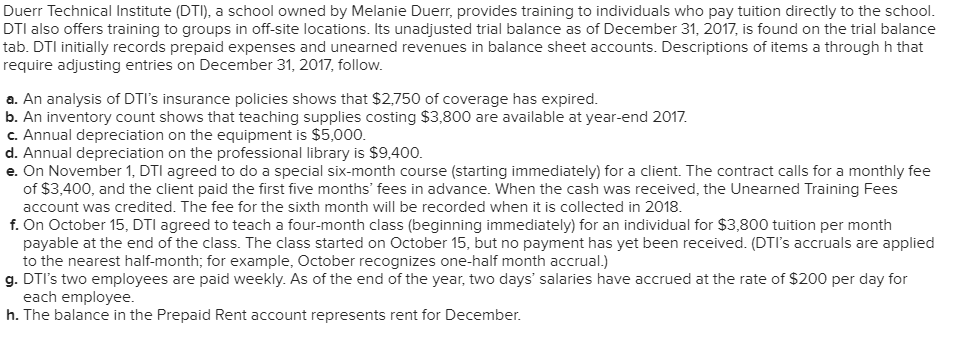

Wanting to have the lowest rate of interest you can? What appears to be a trivial difference at some point saves you far more money, based on how a lot of time you stay in your residence.

Shorter incentives

This really is well-known advantage of transitioning so you’re able to a great 15-season home loan. Thought what you could would when your residence is repaid anywhere near this much sooner! Shortly after lofty desires off capital your infant’s educational costs, upping your senior years contributions, otherwise purchasing an investment property be easily possible.

Disadvantages from a great 15-seasons mortgage

Don’t assume all debtor try an applicant in order to re-finance so you can a good 15-seasons mortgage. However, here are some inquiries to inquire about your self prior to trying in order to a lender.

Ought i pay the repayments? – Tell the truth with on your own: would you manage earmarking significantly more money per month for the financial? Very first, you ought to determine all of your economic visualize. Will be your family income stable adequate to withstand increased payment? In the event the answer is yes, be sure to possess a family https://paydayloanflorida.net/south-highpoint/ savings that will defense step 3-six months regarding costs. Increased percentage of your revenue going with the the house percentage renders a back-up more important.

Am i going to miss the flexibility having collateral? – Individuals almost everywhere was taking advantage of rising home values which have an excellent cash-out refinance. In a nutshell, so it deal comes to taking right out a different sort of home loan which have increased amount borrowed and you may pocketing the real difference (area of the equity) because the bucks. One of several downsides away from refinancing to good fifteen-seasons mortgage is you might not have it quantity of independency along with your security. Consequently, there was a good chance you’ll have to turn to unsecured loans or credit cards to pay for renovations.

Do You will find sufficient currency left-over some other concerns? – Which concern connections back again to the new affordability that a lot more than. Though every person’s economic system varies, just be mindful of all of the mission. Like, does it make sense to help you contribute shorter in order to old-age membership so you can re-finance to help you a good fifteen-year financial? Likewise, have you been comfortable expenses a lot more a lot of money or even more most of the few days on your own home loan whether your rainy date loans actually some the place you want it to be?

Can i eradicate particular income tax gurus? – Do not forget concerning the financial attention taxation deduction you have feel regularly in order to with a 30-season mortgage. Repaying their financial in two the time entails you’ll eradicate that it deduction sooner. Think talking-to a taxation elite group while you are concerned about how good 15-12 months financing could feeling your own taxation liability in the future.

15-season home loan compared to. 30-12 months mortgage

There are many reason the average American resident prefers a great 30-season mortgage. To begin with, permits to own better economic flexibility. The lower fee brings consumers the ability to generate security when you find yourself maintaining other financial obligation payments and you can stashing away bucks getting a crisis.

A suitable candidate to own a good 15-seasons financial generally inspections a few packets: he’s got a stable business no major debt obligations. Since this person are able to afford the higher payment, they would not be wise to allow them to shell out an additional 15 years’ value of focus. But not, create they be better out-of nevertheless with a 30-season financing from the associated tax deductions?

Meanwhile, a candidate having a 30-year financial possess the typical otherwise just underneath-mediocre earnings. Instead of people that are able a fifteen-12 months title, these particular borrowers normally don’t have the resources to manage an excellent notably large homeloan payment. They are apt to have other monetary specifications and you may personal debt instance paying off college loans otherwise performing a family.